Reports of Netflix's death are premature. Very premature

The streaming service is in a better place than its competitors to tackle the financial challenges ahead

The last seven days serve as a reminder why The Dispash was created. You may disagree with the analysis - and I’d be happy if you did - but at least it’s semi-informed non-hyperbole.

Onwards.

Netflix is not dying. A case in how to lose subscribers yet potentially grow profits

Last week Netflix stock fell by 35%. The streaming service lost 200,000 subscribers in the first quarter of 2022, largely in part to suspending operations in Russia, and expects to lose even more this quarter.

Short-term, that could impact investor returns, but doesn't mean that Netflix is about to collapse, although their challenges are a little trickier than just reversing a (possibly temporary) decline in subscriber numbers.

Netflix's headwinds are both unique to their business but also predictable in context of the past two years and the streaming category as a whole. The results can be either seen in isolation (bad) or as part of a bigger picture (far less bad).

What's the current state of play really?

Had Netflix not pulled back from Russia, the streaming service would have shown a 400k+ increase in new users in EMEA and APAC has also grown by over 1m subscribers. That's not too bad for a business built on subscriptions.

Netflix is currently profitable, even if this is a relatively recent development and the company still carries a lot of debt. Currently their operating margin is just over 20%. While their accounting can be a bit creative when it comes to depreciating assets (in this case, content), that's a decent amount of headroom.

TL;DR: Netflix is still making money, just not quite as much as investors hoped for.

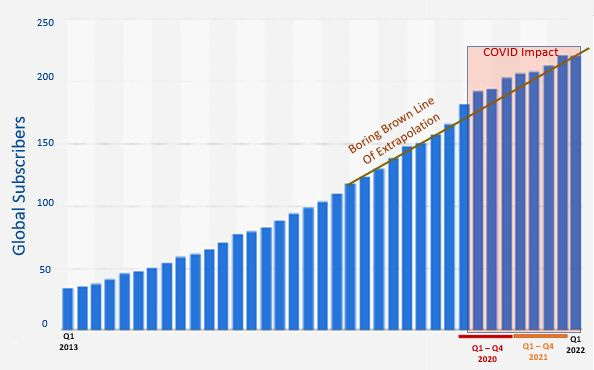

Netflix has slowed down but zoom out and look at their growth line pre and post pandemic (chart below from Mark Ritson). Netflix's growth is course correcting after experiencing a higher than normal subscriber increase during the pandemic.

This isn't a surprise: more people indoors spending less with more time on their hands is likely to lead to more subscription services.

Ritson notes that Netflix's stock may have been in a healthier place if they'd already flagged that their growth over the past two years was fuelled by Covid and would likely slow as the global market started to emerge from the worst of Covid.

People returned to doing normal things, such as meeting friends, going to the restaurant, and watching live sport. Netflix's competition has always been for attention, and for a brief period, large swathes of competition in this space disappeared.

Post pandemic course correction

Netflix's challenge wasn’t exactly hard to predict. Taking a long view was a better way of explaining context as opposed to looking at the effect of the pandemic on certain sectors, which was essential to stay afloat during the pandemic but less useful for planning beyond the pandemic.

Businesses that may have been less compelling in 'normal' times, such as Zoom, suddenly became essential. Peloton offered the perfect product for wealthy households forced inside due to Covid.

The hospitality and aviation industries faced a more immediate existential threat but could be reasonably confident that beyond the pandemic people would still go to restaurants or book flights, albeit perhaps not in the same volumes as before (business flights, for example, may take years to recover to pre-pandemic levels, if at all).

For the industries and businesses affected by the pandemic, survival was the name of the game. Make it through the worst of Covid and they could be reasonably confident business would return. For pandemic businesses, such as Netflix, Zoom, Peloton, and many D2C companies, the question was reversed: what happens when we get to the other side?*

Few companies asked this question. To continue to grow, Peloton needed more people at home with either rising wages or cutting expenses in competing areas, such as the gym. That proposition seemed unlikely and should have been visible in market research. At the time of writing, their stock price sits at $20.39, down from a high of $126.92 nearly 10 months ago.

Zoom happened to be in the right place at the right time, but had a product that wasn't unique. Microsoft and Google simply made their products better and more Zoom-like and bundled them into existing business suites, while a return to the office was an existential threat. An inability to make their product unique is one of the reasons why Zoom's share price has dropped by nearly $300 in the past eight months.

The same is true for many D2C brands. Ecommerce has grown, but people don't dislike bricks and mortar stores, plus delivery returns are costly, scale-ups don't have the same bottomless resources as Amazon, and loyalty is far from assured.

And for Netflix, there was always going to be a finite number of subscribers the company could realistically achieve. The pandemic just saw that number accelerate a little.

The new new new normal

If the pandemic was the "new normal" and the back end of 2021 was the new new normal, then the cost of living crisis is the current reality that brands operate in. And Netflix is possibly best place to emerge from the coming months or even years in first place in its category.

Streaming services are an additional expense. With content fragmented, consumers will have to make choices. This is where the power of Netflix's brand comes into play.

A few days before Netflix's stock market slide, Kantar Worldpanel released a survey that made grim reading for Netflix's competitors. 38% of households were looking to cut back on one SVOD (streaming video on demand service) in order to save money. Amazon Prime and Netflix were described as 'must-haves".

This suggests Netflix is likely to have some protection from subscriber churn, even if it goes for several months without generating a hit series. It also suggests that those who do cancel are more likely to be back.

It also allows Netflix to play with price elasticity. The streaming service has been steadily increasing prices over the past 12 months. The "must have" rating gives Netflix more leeway than competitors to keep the 20% profit margin in place before looking into other options to keep revenue, profit and loss steady.

And Netflix has options. Converting password sharers into new subscribers, or at least upgrading them into existing accounts is easier than building out an ad-tech platform, which is something that currently sits outside of the business's core capabilities.

When (not if) adverts do arrive, Netflix can experiment with cheaper plans subsidised by adverts or can limit inventory and charge a premium.

So, yes, options, largely powered by the brand. Premium inventory on Netflix will be worth more than a second tier streaming service or a competitor that allows advertising at a flat subscription price.

And streaming is a sector that faces an interesting - or rough, depending on your viewpoint - few years ahead.

It’s easy to cancel and isn’t essential. The options for survival are to view it as an added extra that doesn’t need to make money (Amazon, Apple), build up a catalogue of valuable IP (Disney), or invest in content and hope to keep turning out hits (everyone else).

Looking at these strategies, Netflix has the most to lose. But it starts from a stronger position than many competitors.

So is Netflix dying? At this stage, it’s vital signs are positive, but it’s worth taking a health check in 12 months.

*Given infection numbers and deaths, you can rightfully argue that we're not over Covid. But in terms of human behaviour and economics, we're probably a little closer to the final stages.

Interesting reading

A brief analysis of Musk and Twitter

Assuming the deal is finalised, Elon Musk is set to own Twitter, a piece of news that’s somewhat disproportionate to the coverage it receives. Musk clearly has a vision of sorts for Twitter that may or may not be close to the interviews he’s given. Tesla and Space X are physical products in sectors that are regulated or have overriding safety concerns. PayPal also operated in a regulated sector. Twitter is a very different type of product that has to serve a lot of different masters.

Does a very busy owner who specialises in other sectors have what it takes to oversee advertiser products. And if not advertising, then what? Car safety regulations are largely the same in most jurisdictions, but Europe may choose to enact regulations differently to the USA or a more autocratic country such as India. How does the commitment to free speech balance against adult content? Or Germany’s Holocaust laws? Or harassment of minorities? The people who enforce moderation decisions are often lower paid, lower grade employees or contractors, often dealing with more nuance than Musk’s free speech absolutionist position would imply. No link here, just a lot of questions. This could make Twitter a better product or end up being an extremely expensive folly.

D2C is not really making any money

Direct To Consumer has a lot of people very excited, generated a lot of VC money and has largely been built on cheap digital performance advertising that’s getting more expensive. Now investors are looking for a return and D2C companies have to worry about the same thing as other companies, such as profit and margin. Wholesale and physical stores aren’t sexy, but they offer scale and a part to profitability, while investing in brand typically gives better long-term results. We’re about to come full circle here. LINK. Bonus link: SUBSCRIPTION FATIGUE.

Subscriptions aren’t a publishing business model

Publishers pivoted to subscriptions as a way to generate revenue because Facebook had taken their ad dollars and could destroy business models at a whim. But over-reliance on subscriptions can leave you at the mercy of an audience who are looking to preserve their cash and it limits the ability to use the best part of the product as a selling tool. Brian Morrissey is very good on this.

Snapchat trends

Snapchat is a fascinating company. It’s found its own niche away from TikTok, Instagram and other networks without generating much buzz recently. Their generations trends report points towards a few longer-term trends, which are a bit harder to articulate such as moving away from sharing to large audiences to tools that put the user back in control. Snap is quieter than other networks in the press, but that may not be a bad thing. LINK.

Returning to the office isn’t even a debate in certain sectors

A thoroughly depressing but probably accurate picture from Vox on jobs that haven’t seen any of the pandemic benefits and wouldn’t be able to work from home even if they wanted to. There’s more to this debate, especially around class and affluence, than narrow view thought leaders on LinkedIn telling us remote work is the future. LINK.

More virtual cola

Pepsi is bullish on NFTs. The Pepsi Mic Drop NFTs was a nice project that had a little more thought about it than some Web3 campaigns. How it generates brand equity, which seems to be the intention judging by The Drum’s piece, is a little bit beyond me. Does this really help to build ESOV, long-term memories and preference that eats into Coke’s sales rather than, say, a mix of TV and YouTube? Pepsi had a good start to the decade because they advertised while Coke pulled back. I don’t know Pepsi’s strategy but this feels like a lot of work to market to a very niche audience. LINK.

Thanks for reading this far. Hopefully you’ve found it mildly diverting. Like what you’ve read? Forward it onto somebody and ask them to subscribe.

It’s been a Hall & Oates kinda week. So playing us out this week: Kiss On My List. Although just stick on the Greatest Hits album if you want a good working soundtrack.